List To Floor Assertion

Financial Statement Analysis Example Financial Statement Analysis Financial Statement Analysis

9 Assertion Hallway Concepts That Will Deliver The Thoroughfare To Life 2020 In 2020 Living Room Reveal Beach House Decor Hallway Decorating

Pin On Customer Experience

Chapter 9 Audit Procedures

Pin On For Me Resilience

Distinct Furniture Along With Modern Pattern Makes An Assertion In Your Home Come Across Present Day Settees Areas And Me Home Home Remodeling House Interior

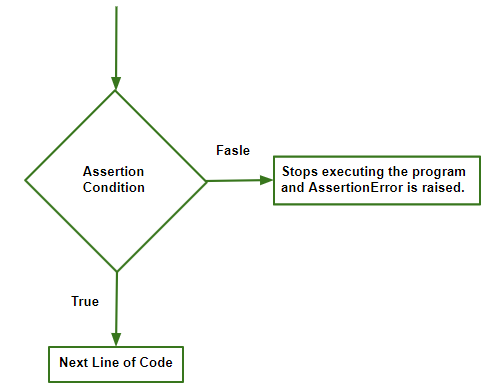

For example in order to think you typically begin with what you know to be true the following are illustrative examples of assertions.

List to floor assertion. To test the occurrence of. Assertions regarding the recognition measurement and presentation of assets liabilities equity income expenses and disclosures in accordance with the applicable financial reporting framework e g. During your audit you need to test management financial statement assertions for fixed and intangible asset transactions. The six assertions that you must attend to when auditing occurrence ownership completeness authorization accuracy and cutoff are outlined here occurrence.

List of audit assertions related to account balances 1 existence. In addi tion to the components of every constraint descriptor an assertion. These assertions are as follows. In preparing financial statements management is making implicit or explicit claims i e.

4 10 4 assertions an assertion is a named constraint that may relate to the content of individual rows of a table to the entire contents of a table or to a state required to exist among a number of tables. The assertion of accuracy and valuation is the statement that all figures presented in a financial statement are accurate and based on proper valuation of assets liabilities and equity balances. This assertion is critical for the asset accounts because it is a reflection of the strength of the company. Occurrence tests whether the fixed asset transactions actually took place.

Management assertions are claims made by members of management regarding certain aspects of a business. Financial statement assertions are claims made by an organization s management regarding its financial statements. The concept is primarily used in regard to the audit of a company s financial statements where the auditors rely upon a variety of assertions regarding the business. It refers to the fact that the assets the liabilities and the equity balances mentioned in the books exist at the end of the accounting period.

For example if a balance sheet of an entity shows buildings with carrying amount of 10 million. This is a basis for logic thought processes and systems. An assertion is described by an assertion descriptor. The assertions form a theoretical basis from which external auditors develop a set of audit procedures.

Python Assertion Error Geeksforgeeks

100 Opposite Words List Antonym Vocabulary Example Sentences In 2020 Opposite Words Opposite Words List Vocabulary

A Literary Review Is A Summary About A Specific Topic In Essay Form Contains A Apa Re Argumentative Essay Creative Writing Workshops College Admission Essay

Small Bathroom Design Photos Low Budget Small Bathroom Design Photos Low Budget Small Bathroom In 2020 Budget Bathroom Remodel Bathrooms Remodel Diy Bathroom Remodel

Https Comptroller Defense Gov Portals 45 Documents Fiar Fiar Guidance Pdf

Profit And Loss Statement Self Employed Profit And Loss Statement Statement Template Budgeting Worksheets

Wandfarbe Apricot Flur Gestalten Floraler Teppichl Ufer Decorstyle Entrywaydecor Decorsmall In 2020 Narrow Entryway Decor Foyer Decorating Hallway Designs

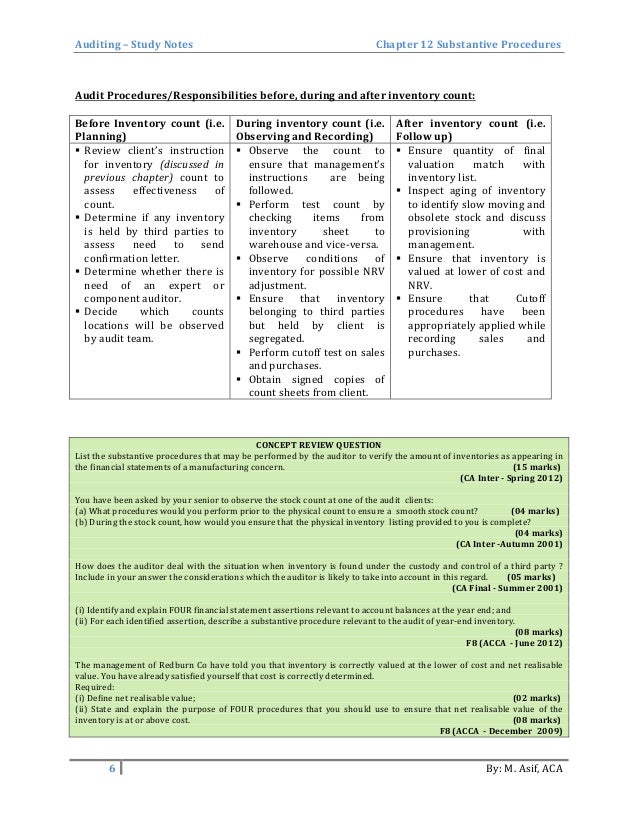

Substantive Procedures Auditing Study Notes

Public Mind Map By Tyler Smith Create Your Own Collaborative Mind Maps For Free At Www Mindmeister Com Mind Map Eos Tyler Smith

Ana Book Blogger On Instagram How Do You Guys Store Your Books Towering Bookshelves Or Stacke In 2020 Study Room Decor Bookshelves In Bedroom Room Ideas Bedroom

Distinct Furnishings Along With Advanced Plan Makes An Assertion In Your Home Look Up New Chairs Mattress And Sto Murphy Bunk Beds Bunk Beds Murphy Bed Plans

A Visit To Rumson Vintage House Plans Luxury House Plans Rumson

Check Out These Out Of This World Approaches With Regard To A Triple Bunk Bed Space Bunkbedcabin Bunk Beds Triple Bunk Beds Modern Bunk Beds